Smart Office Market Size Projected to Reach USD 161.73 Billion by 2032

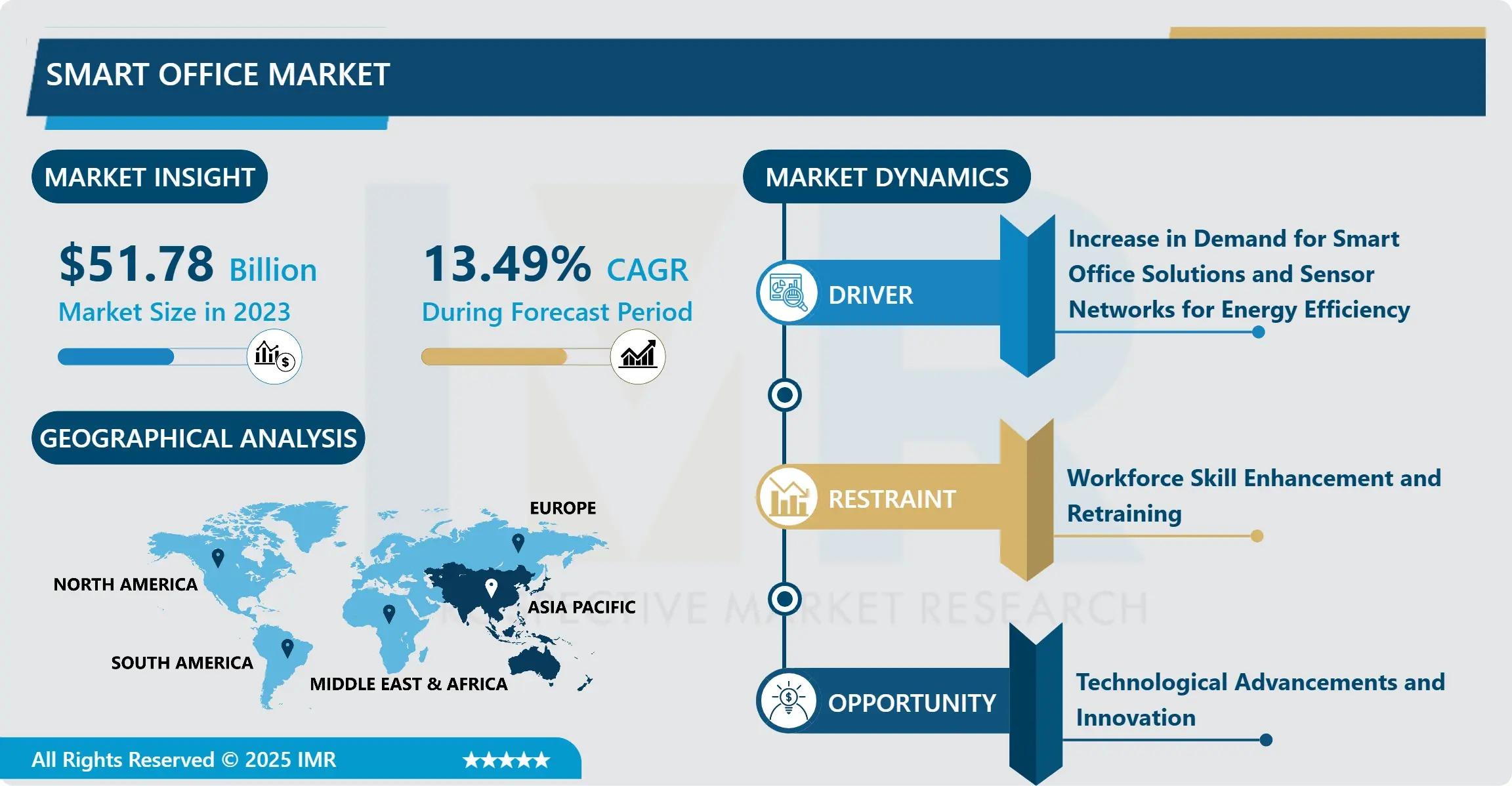

According to a new report published by Introspective Market Research, Smart Office Market by Component, Product Type, Office Type, and Region, The Global Smart Office Market Size Was Valued at USD 51.78 Billion in 2023 and is Projected to Reach USD 161.73 Billion by 2032, Growing at a CAGR of 13.49%.

Introduction / Market Overview:

The global smart office market is at the intersection of real estate, technology, and human resources, focused on creating intelligent, connected, and data-driven workplace environments. This market encompasses a suite of IoT-enabled hardware, software, and services that automate and optimize building operations and employee experiences. The core advantage of a smart office over a traditional workspace lies in its ability to harness data from sensors and devices to enhance operational efficiency, slash energy consumption, boost employee productivity and well-being, and enable flexible, hybrid work models. By moving from static to dynamic environments, smart offices create responsive ecosystems that adapt in real-time to occupancy and usage patterns.

Smart office solutions are deployed across various commercial real estate segments and corporate industries. Key applications include automated lighting and HVAC control, advanced security and access management, smart meeting room booking systems, occupancy and space utilization analytics, and employee-centric applications like wayfinding and desk booking. Major industries driving adoption include corporate enterprises across IT, finance, and professional services; co-working and flexible office space providers; government facilities; and healthcare and educational campuses, all seeking to create safer, more efficient, and more attractive workplaces in a post-pandemic, hybrid work era.

Growth Driver:

The paramount growth driver for the smart office market is the permanent global shift towards hybrid and flexible work models, accelerated by the COVID-19 pandemic. As companies adopt a mix of remote and in-office work, they require intelligent office infrastructure that maximizes the utility of shared spaces and supports seamless collaboration. Smart office technologies, such as IoT sensors for space utilization, hot-desking applications, and advanced video conferencing systems, are essential for managing a dynamic, fluid workforce. These solutions allow organizations to optimize real estate footprint, reduce costs, ensure a safe and productive environment for employees who choose to come in, and provide data-driven insights to inform workplace strategy, making smart office adoption a strategic imperative rather than a luxury.

Market Opportunity:

A significant market opportunity lies in the integration of artificial intelligence (AI) and machine learning (ML) with smart office platforms to create predictive and truly cognitive workplaces. Moving beyond basic automation and monitoring, AI can analyze data from myriad sensors to predict peak occupancy, pre-emptively adjust environmental controls for comfort and energy savings, automate administrative tasks like meeting summaries, and even provide personalized workspace settings for employees. Furthermore, the rise of "smart building-as-a-service" (BaaS) models presents a compelling opportunity for providers to offer integrated, subscription-based solutions that bundle hardware, software, and management, lowering the upfront capital barrier for enterprises and creating recurring revenue streams in this rapidly evolving market.

Title: Smart Office Market, Segmentation

The Smart Office Market is segmented on the basis of Component, Product Type, and Office Type.

Component

The Component segment is further classified into Hardware, Software, and Services. Among these, the Hardware sub-segment accounted for the highest market share in 2023. Hardware, including IoT sensors, smart lighting fixtures, connected HVAC controllers, and access control readers, forms the foundational physical layer of any smart office. The initial capital expenditure for installing this extensive network of interconnected devices is substantial, driving the segment's revenue dominance. As the essential "nervous system" that collects environmental and occupancy data, hardware investments are the critical first step in any smart office deployment.

Product Type

The Product Type segment is further classified into Intelligent Lighting, Security & Access Controls, HVAC Control Systems, and Audio-Video Conferencing Systems. Among these, the Security & Access Controls sub-segment accounted for the highest market share in 2023. This dominance is driven by the non-negotiable need for physical security in commercial buildings, now enhanced with smart capabilities like biometric access, mobile credentialing, and integrated visitor management. The convergence of traditional security with IoT and data analytics to create safer, more seamless, and audit-ready access environments represents a high-priority, high-value investment for organizations, fueling this segment's growth.

Some of The Leading/Active Market Players Are-

• Schneider Electric SE (France)

• Siemens AG (Germany)

• Johnson Controls International plc (Ireland)

• Honeywell International Inc. (US)

• Cisco Systems, Inc. (US)

• ABB Ltd. (Switzerland)

• Legrand S.A. (France)

• Lutron Electronics Co., Inc. (US)

• Crestron Electronics, Inc. (US)

• Signify N.V. (Netherlands)

• Robert Bosch GmbH (Germany)

• IBM Corporation (US)

• Microsoft Corporation (US)

• Oracle Corporation (US)

• “and other active players.”

Key Industry Developments

News 1:

In April 2024, Siemens launched its next-generation "Siemens Xcelerator for Buildings" platform, featuring enhanced AI-driven analytics for predictive space and energy management in smart offices.

The open digital business platform is designed to simplify and accelerate the digital transformation of buildings, offering scalable solutions from single sites to global portfolios.

News 2:

In March 2024, Cisco and Johnson Controls announced an expanded strategic partnership to integrate Cisco's collaboration devices and networking infrastructure with Johnson Controls' OpenBlue smart building platform.

The collaboration aims to deliver a unified, secure, and immersive hybrid work experience, seamlessly connecting physical building systems with digital collaboration tools.

Key Findings of the Study

• Hardware is the dominant component, and Security & Access Controls lead the product type segment.

• North America is the largest regional market, driven by high technology adoption rates, a strong commercial real estate sector, and the presence of leading technology vendors.

• The global shift to hybrid and flexible work models is the primary market growth driver.

• Major trends include the integration of AI/ML, the rise of smart building-as-a-service models, and a focus on occupant health and well-being analytics.